The post Crown Castle Dividend Cut: The Factors Behind the Reduction appeared first on Dividend Power.

Crown Castle Inc. (CCI) reduced its dividend due to the impact of the T-Mobile and Sprint merger, increased competition, financial leverage, and technological advancements. Lower rental revenue resulted in weaker results. The firm froze its dividend in Q4 2022 and eventually cut it this year.

The share price has fallen dramatically since the end of 2021. Investors sold this dividend stock due to concerns about leverage, poor results, and a potential dividend cut, as safety concerns increased. Depending on future results, another reduction may occur.

Overview of Crown Castle Inc.

Crown Castle Inc. was founded in 1994 and is headquartered in Houston, TX. It is structured as a real estate investment trust (REIT), specifically a telecom tower REIT. The trust owns, operates, and leases approximately 40,000 cell towers, 90,000 route miles of fiber, and about 105,000 small cells on air or under contract. The majority of its tower assets are in metropolitan areas or along highway corridors.

Total revenue was $6,568 million in 2024 and $6,468 million in the past twelve months. Most of the revenue is derived from site rentals.

Dividend Cut Announcement

During the second quarter of 2025, on Wednesday, May 21st, Crown Castle Inc. (CCI) cut its dividend. The company’s quarterly dividend rate was $1.565 per share before the announcement. The dividend is now $1.0625 per common share, a 32.1% reduction. In the announcement on May 21st, the trust stated,

“…that its Board of Directors has declared a quarterly cash dividend of $1.0625 per common share. The quarterly dividend will be payable on June 30, 2025 to common stockholders of record at the close of business on June 13, 2025. Future dividends are subject to the approval of Crown Castle’s Board of Directors.”

In the second quarter earnings release, the REIT stated,

“Common stock dividend. During the quarter, Crown Castle paid common stock dividends of approximately $463 million in the aggregate, or $1.0625 per common share, a decrease of 32% on a per share basis from the same period a year ago.”

Later, in the second quarter earnings call transcript, the Interim President & CEO stated,

“In the second quarter, we made progress implementing our capital allocation framework by decreasing our dividend per share to $4.25 on an annualized basis, which will increase our financial flexibility going forward. Following the close of our sale transaction, we intend to grow the dividend in line with AFFO excluding amortization of prepaid rent by maintaining a payout ratio of 75% to 80%.”

Effect of the Change

By executing a 32% dividend cut, Crown Castle aimed to reduce its quarterly and annual distributions, thereby increasing its financial flexibility. The firm is experiencing competitive pressures and a negative impact on demand from the merger of T-Mobile and Sprint. Additionally, the balance sheet is leveraged.

The REIT’s dividend rate has been constant since Q4 2022, so it did not have a streak of increases. However, before that freeze, Crown Castle consistently increased the dividend. The result is that less free cash flow is required for the dividend distribution, allowing the retailer to focus on its core tower business and reduce debt.

Challenges

Crown Castle is facing a challenging business environment due to the T-Mobile and Sprint merger, increased competition, and heightened leverage.

T-Mobile and Sprint Merger

In 2020, T-Mobile and Sprint merged, forming a larger wireless company with a focus on a 5G network. The Sprint brand was essentially discontinued and merged into T-Mobile. This merger had a significant impact on Crown Castle, as it lost a customer. Its towers no longer needed to support equipment for two separate companies. After the event, Sprint began a process of cancelling tower leases that is still affecting the trust. In fact, rental revenue peaked in 2023 and declined in 2024. The Spring Cancellations are still negatively impacting revenue in 2025.

Competition

Crown Castle faces significant competition from other tower rental REITs. It is the number two REIT behind American Tower (AMT), which did not cut its distribution. The other major player is SBA Communications Corporation (SBAC). However, indirect competition is increasing with the emergence of satellite, independent tower companies, and fiber optic and small cell networks. Rising competition will affect demand.

Debt and Leverage

Crown Castle is a leveraged firm with over $29 billion in net debt. It currently has roughly 2.44 times interest coverage and about a 6.03 times leverage ratio. However, it has an investment grade credit rating of BBB/Baa3 because the firm has cut its dividend and is divesting its fiber and small cell business.

Dividend Safety

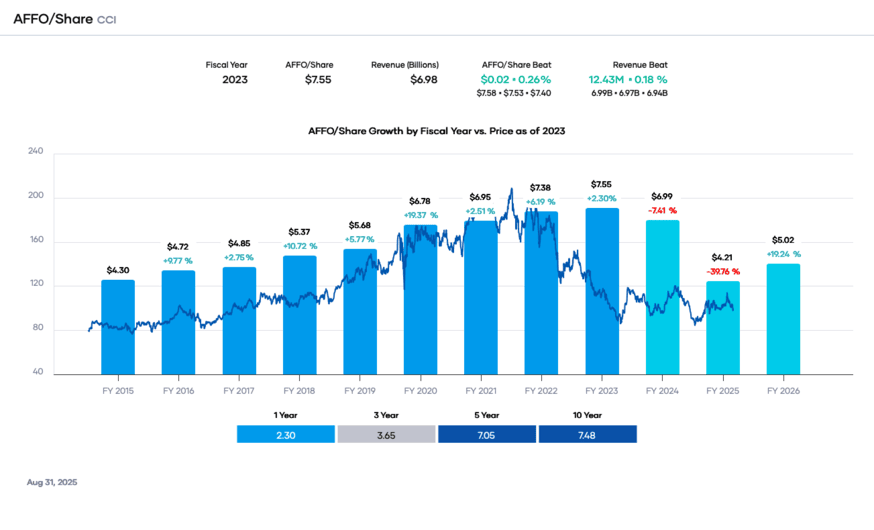

Despite generally rising revenue and earnings per share (“EPS”), Crown Castle’s dividend safety was low because of poor safety metrics. AFFO per share exhibited a rising trend, peaking in 2023 at $7.55. However, it declined in 2024 to $6.99 per share, and is expected to fall further in 2025 to $4.21 per share.

{kind=link}

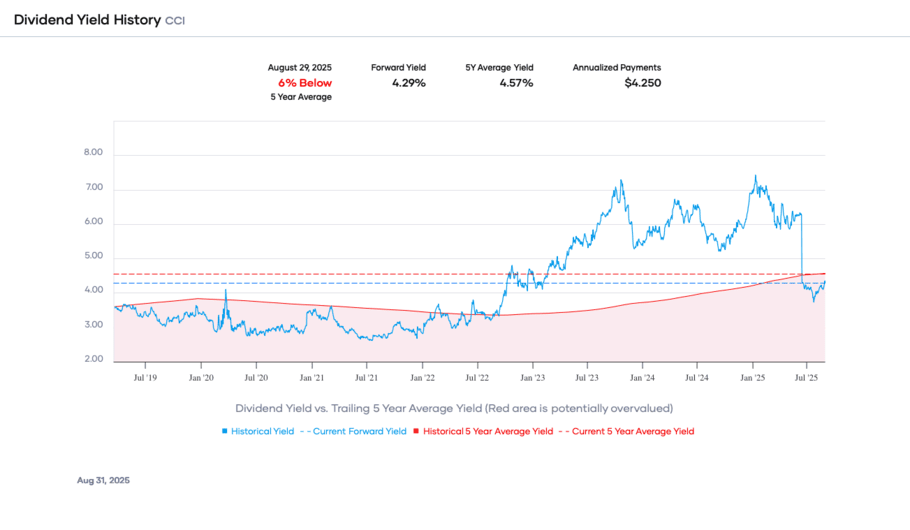

As seen in the chart below from Portfolio Insight*, the dividend yield climbed rapidly to over 7%. Although not high for a REIT, this value, combined with the rapid rise, suggests poor operating results. It was much greater than the 5-year average of 4.57%. After reducing the dividend by approximately 32%, the forward dividend yield is now around 4.29%. The quarterly rate is $1.0625 per share. However, the yield is still appreciably higher than that of the S&P 500 average.

{kind=link}

The annual dividend now requires about $1,848.75 million ($4.25 yearly dividend x 435 million shares), compared to $2,723 million in 2024. In addition, based on consensus 2025 estimates of $4.21, the estimated dividend to AFFO/S payout ratio will be over 100%. We expect the annual difference in cash flow requirements to enhance liquidity. The trust has indicated it will use the cash flow for share buybacks and invest in the business.

Although the dividend is in a better position and more secure now, the firm’s dividend is not entirely safe. Further decline in demand, poor operating results, or technological change may result in another dividend cut. That said, the credit rating agencies are positive.

In addition, the restaurant firm receives a dividend quality grade of ‘F’ from Portfolio Insight. Hence, Crown Castle is in the bottom percentile of dividend stocks tracked. We view the equity as at risk for another dividend cut unless the results improve.

Final Thoughts on Crown Castle (CCI) Dividend Cut

Before the T-Mobile and Sprint merger, Crown Castle was a dividend growth stock with an increasing annual dividend. However, the merger affected rental demand and interrupted the streak, ultimately reducing the payout this year. The merger’s effects, competition, leverage, and technological change have created challenges for the tower rental REIT. The dividend safety metrics were relatively poor. As a result, Crown Castle cut its dividend. However, we view the REIT as at risk for another reduction.

Related Articles on Dividend Power

Jack in the Box: Dividend Payout Suspended to Reduce Debt

4 Dividend stocks to Buy in Fall 2023

The post Crown Castle Dividend Cut: The Factors Behind the Reduction appeared first on Dividend Power.