The post Alexandria Real Estate: Analyzing the Dividend Cut appeared first on Dividend Power.

Alexandria Real Estate Corporation (ARE) cut its dividend due to the impact of a weakening life science real estate market, federal policy and budget changes, high interest expense, and other factors. Weak financial results in 2025 and a weak outlook for 2026 are also a concern. The firm was a Dividend Contender with a 14-year streak of annual increases before the cut.

The share price plunged 10% the day the dividend cut was announced and fell further since then. Investors sold this dividend stock after the announcement, and sentiment remains negative. Depending on future operating and financial results, another reduction may occur.

Overview of Alexandria Real Estate Equities

Alexandria Real Estate Equities was founded in 1994 and is headquartered in Pasadena, CA. It is a real estate investment trust (REIT) focusing on life science buildings. The trust’s life science campuses and buildings are located in urban science and innovation clusters, including the Bay Area, San Diego, Seattle, Boston, New York City, Maryland, and the Research Triangle. At the end of December 2025, the REIT had 35.9 million square feet of properties. The REIT also offers venture capital financing to companies.

Total revenue was $2,945 million in 2025 and in the past twelve months.

Dividend Cut Announcement

During its Analyst and Investor Day on Wednesday, December 4th, Alexandria Real Estate Inc. (ARE) cut its dividend. The company’s quarterly dividend rate was $1.32 per share before the announcement. The dividend is now $0.72 per common share, a 45.5% reduction. In the announcement, the REIT stated,

“The board’s decision to reduce the declared dividend per common share reflects the company’s commitment to fortify its already strong balance sheet, enhancing financial flexibility and preserving liquidity of approximately $410 million on an annual basis. In addition to conserving significant capital, the dividend provides an attractive yield on its common stock of 5.4%, based on the closing stock price on December 1, 2025.”

Later in the transcript of the Investor Day, the CEO stated,

“Moving from left to right in the blue shading there, we expect to solve that $2.7 billion funding need with 2 strategies. First, our Board approved a reduction of the dividend of 45% today, which will generate an additional $410 million of capital that can be used to address our funding needs. And then second, we plan to address the $2.3 billion remainder with both dispositions of noncore assets and land, and sales of partial interest of core assets.”

“Next, I want to provide some context around the change to the dividend that was considered by the Board. The Board considered a variety of factors, including taxable income, our AFFO coverage ratio, current and future capital needs, the potential for $410 million of additional capital and our dividend yield. Following the dividend cut, the dividend yield is much more in line with the average of other S&P 500 REITs, as you can see on this slide. Including the dividend reduction announced today, net cash flows from operations after dividends and distributions is expected to be $525 million at the midpoint of our guidance for 2026, and will represent a significant component of our overall funding need — our overall funding plan.”

Effect of the Change

By cutting the dividend by almost 46%, Alexandria Real Estate desired to decrease its quarterly and annual dividend distributions and address its need for liquidity and funding, while shoring up its balance sheet. The trust needs $2.7 billion in excess of its construction needs to pay down debt.

The REIT was a dividend growth stock with a 14-year streak of increases, making it a Dividend Contender. The result is that less free cash flow (“FCF”) is required for the dividend distribution, allowing the company to use the funds for paying debt.

Challenges

Alexandria Real Estate is facing a challenging business environment because of a soft life science building demand. Federal government policy changes, budget cuts to life science funding, a government shutdown, and reduced venture capital funding have affected life science companies.

Policy Changes

The National Institute of Health (NIH) has changed its policy for indirect costs. The funding agency has capped indirect cost rates to 15%, reducing the ability to pay for items such as rent and other administrative costs. Next, the U.S. Food & Drug Administration (FDA) has experienced personal turnover and staffing cuts affecting its ability to evaluate submissions. Lastly, a broader push by the federal government to lower drug costs has curbed reimbursements.

Too Much Real Estate

The COVID-19 pandemic resulted in significant investment in life science buildings. However, demand has not kept up with the pace of construction. Consequently, occupancy rates are declining, affecting cash flow for REITs. Specifically, Alexandria Real Estate is expecting an occupancy decline into the high-80% range, much lower than its historical norm.

Weak 2026 Outlook

Alexandria Real Estate issued a weak outlook for 2026 based on current market trends. It expects reduced funds from operations (FFO) of $6.26 to $6.55, an occupancy decline into the high-80% range, lease expirations, weakening rental spreads, and lower capitalized interest, higher interest expenses, and reduced investment gains.

Dividend Safety

Because of weaker revenue and earnings per share (“EPS”) in 2025, Alexandria Real Estate’s dividend safety metrics have weakened. EPS was negative in 2025 because of lower occupancy, less revenue, and impairment charges. They were a loss of ($8.44) in 2025. Consensus estimates indicate $6.42 per share in 2025.

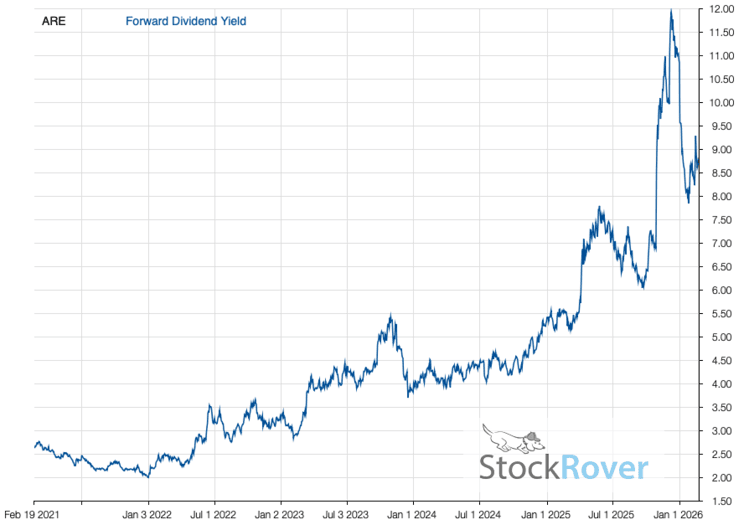

Source: Stock Rover

As shown in the chart below from StockRover*, the dividend yield increased rapidly to almost 12% in late 2025. This value is over 10%, which is associated with companies facing operating and financial difficulties. Also, it was much greater than the 4-year average of 4.79%. After reducing the dividend by approximately 46%, the forward dividend yield is now around 5.37%. The quarterly rate is $0.72 per share. However, the yield is still appreciably greater than that of the S&P 500 average.

{kind=link}

The annual dividend now requires about $489.6 million ($2.88 yearly dividend x 170 million shares), compared to $911 million in 2025. The lower rate will improve the payout ratio, which was usually high for REITs. Additionally, net cash flow from operations will improve. We expect the yearly difference in cash flow requirements to enhance liquidity and allow Alexandria Real Estate to pay down debt.

Although the dividend is in a better position and more secure now, the firm’s dividend is still not entirely safe, as demonstrated by the soft 2026 outlook. Further decline in demand, more federal budget cuts to life science companies, and changing policies may result in another dividend cut.

Hence, we view the equity as at risk for another dividend reduction.

Final Thoughts on Alexandria Real Estate (ARE) Dividend Cut

A weakening life science real estate market has negatively affected occupancy, revenue, cash flow, and profitability. In addition, high interest rates and expenses are headwinds. As a result, a weak outlook for 2026 and possibly into 2027 has caused difficulties for Alexandria Real Estate. The collective effect resulted in declining dividend safety metrics. As a result, Alexandria Real Estate cut its dividend. However, we view the company as at risk for another significant decrease.

Related Articles on Dividend Power

Alexandria Real Estate (ARE): Undervalued REIT

The post Alexandria Real Estate: Analyzing the Dividend Cut appeared first on Dividend Power.