The post 3 Top Dividend Stocks For 2026 appeared first on Dividend Power.

It is an opportune time for investors to reassess their portfolios for 2026. The S&P 500 Index wrapped up another strong year in 2025, registering a return of approximately 19%.

The good news is that there are still undervalued stocks with strong dividends to choose from, despite the market’s strong performance last year.

The following 3 Dividend Aristocrats have increased their dividends for over 25 years. They also have total expected returns above 10% per year, making them among our top dividend stock picks for 2026.

Top Dividend Stocks for 2026

Becton Dickinson & Co. (BDX)

Becton, Dickinson & Co. is a global leader in the medical supply industry. The company was founded in 1897 and has 75,000 employees across 190 countries. The company generates about $20 billion in annual revenue, with approximately 43% of revenues coming from outside of the U.S.

BD also reported results for the fourth quarter and fiscal year 2025, which ended September 30th, 2025. For the quarter, revenue grew 8.3% to $5.89 billion, but this was $20 million below estimates. Adjusted earnings-per-share of $3.96 compared favorably to $3.81 in the prior year and was $0.05 more than expected. For the fiscal year, revenue grew 8.2% to $21.8 billion, while adjusted earnings-per-share of $14.40 compared to $13.14 in FY 2024.

BD provided an outlook for fiscal year 2026 as well. Revenue is projected to grow at a low single-digit rate. Adjusted earnings-per-share are expected to be in a range of $14.75 to $15.05. At the midpoint, this would represent growth of 3.5% from FY 2025.

BD has increased earnings-per-share 5.9% per year over the past decade and has grown earnings in 7 out of the last 10 years. We now forecast that BD can grow earnings at a rate of 5% per year through fiscal 2031.

BD showed that it can perform well in less-than-ideal economic conditions during the last recession. The company’s key competitive advantage is that its products are in high demand as medical devices and other healthcare products are still sought out during a recession. People will seek medical care regardless of how the economy is performing.

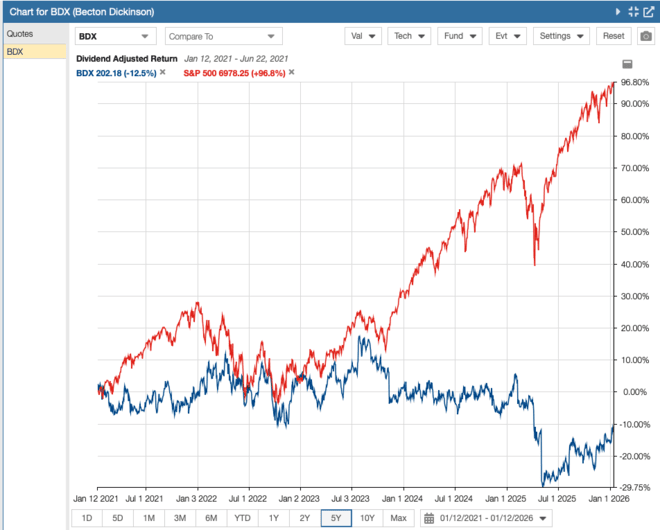

This ability to grow or maintain earnings in any economic climate makes BD a quality company and a safe dividend payer. On November 6th, 2025, BD increased its quarterly dividend 1.0% to $1.05, extending the company’s dividend growth streak to 54 consecutive years, making it a Dividend King. According to Stock Rover, the share price is down nearly 13% in the past 5-years.

{kind=link}

Nordson Corp. (NDSN)

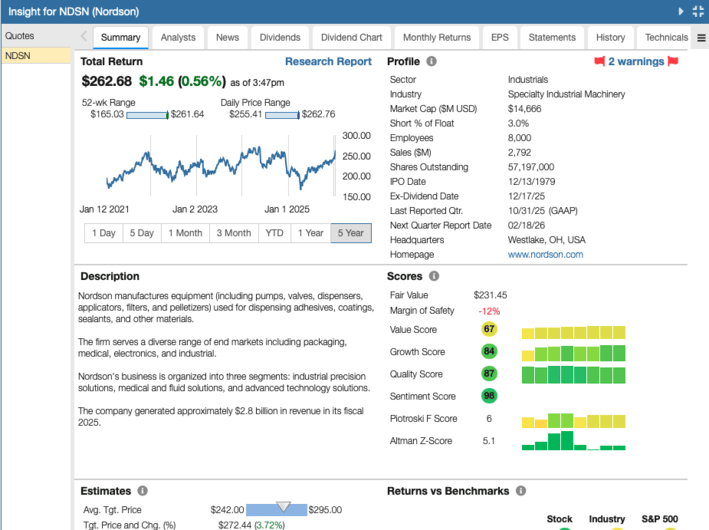

Nordson has operations in over 35 countries and engineers, manufactures, and markets products used for dispensing adhesives, coatings, sealants, biomaterials, plastics, and other materials, with applications ranging from diapers and straws to cell phones and aerospace. The company generated $2.7 billion in sales last fiscal year.

On December 10th, 2025, Nordson reported fourth quarter results for the period ended October 31, 2025. For the quarter, the company reported sales of $752 million, 1% higher compared to $744 million in Q4 2024, driven by a 2% favorable forex translation and a 1% positive acquisition impact.

The Medical and Fluid Solutions segment saw sales increase by 10%, while Industrial Precision Solutions and Advanced Technology revenue fell 2% and 4%, respectively. The company generated adjusted earnings per share of $3.03, a 9% increase compared to the same period in the prior year.

From FY 2016 through FY 2025, Nordson grew earnings-per-share by a solid 9.1% annually. In the last five years, however, this growth has sped up to 13.3% per year. Earnings dipped in the previous recession and fell again in 2020, but the company rebounded sharply and produced impressive results in 2021 and beyond.

Nordson outlines an investment thesis for itself, citing best-in-class technology that boosts client output while lowering costs, a worldwide service model, a balanced income stream, and an exceptional business track record. Areas for growth include increased use of disposable products, productivity investments, mobile computing, increased medical device usage, and lightweight/lean manufacturing of vehicles, all of which benefit from the company’s adhesive and coating segments.

Additionally, with the acquisitions of CyberOptics Corporation and Atrion, Nordson has expanded its position in the semiconductor and electronics industries and proprietary medical products.

NDSN has increased its dividend for 62 years.

{kind=link}

Cintas Corporation (CTAS)

Cintas Corporation is the U.S. industry leader in uniform design, manufacturing & rental. The company also offers first aid supplies, safety services, and other business-related services. Cintas was founded in 1968 and has annual revenues of more than $10 billion.

Cintas posted second quarter earnings on December 18th, 2025, and results were slightly better than expected on both the top and bottom lines. The company posted $1.21 in earnings-per-share, which was two cents ahead of estimates. Revenue rose 9.4% year-over-year to $2.8 billion, beating estimates by $30 million. Operating income came to $656 million, while net income was $495 million, up 11% year-over-year. Free cash flow was $425 million, up 24% year-over year. Capex was $106 million, while $86 million was spent on acquisitions.

Dividends were $182 million, while share repurchases were $623 million. Gross margin for Uniform Rental Facility Services was 49.8% of revenue, 57.7% of revenue for First Aid and Safety Services, 48.2% for Fire Protection Services, and 41.9% for Uniform Direct Sale. Guidance for the year was raised to $11.15 billion and $11.22 billion for revenue, while earnings are expected to rise to $4.81 to $4.88 per share.

Cintas has compounded its earnings-per-share at a rate of about 16% annually since 2012. Over full economic cycles, we believe the company can deliver continued earnings growth in the range of 10% per year. Cintas’ two primary growth levers are higher organic revenue and higher margins. Cintas has proven it can grow revenue consistently over the years. It is also adept at removing cost redundancies, which drives operating margin higher over time.

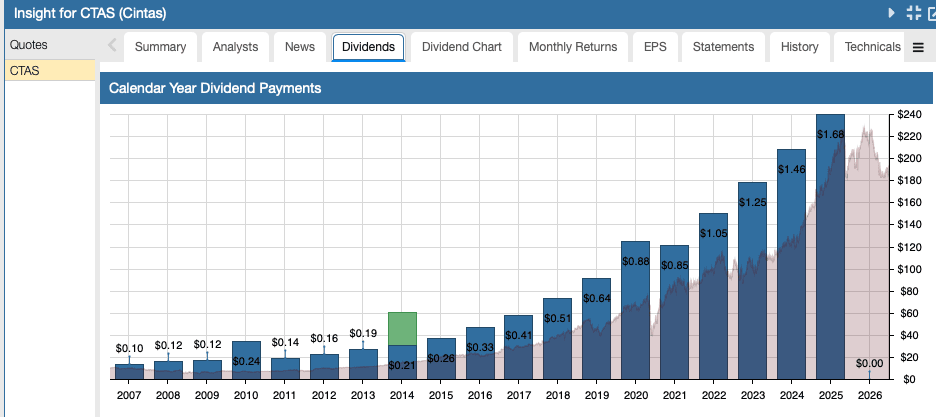

Cintas qualifies to be a member of the Dividend Aristocrats Index with an impressive 43 years of consecutive dividend increases. Cintas’ payout ratio has always been quite low, and that is no different today. We see the dividend remaining under 40% of earnings for the foreseeable future, with years of steady increases on the way.

{kind=link}

Disclosure: No positions in any stocks mentioned.

Related Articles on Dividend Power

3 Blue Chip Dividend Stocks to Play Defense

Our Top Dividend Aristocrat Picks in July 2024

The post 3 Top Dividend Stocks For 2026 appeared first on Dividend Power.